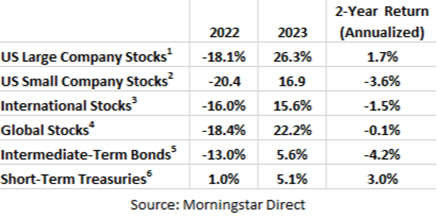

The last two years were quite a whirlwind for financial markets. Investors experienced a wide range of emotions with high volatility in both stock and bonds. However, interestingly, if an investor went to sleep at the start of 2022 and woke up again two years later at the start of 2024 it may have appeared very little time passed at all by looking at the financial markets (except for the dramatic increase in interest rates). This round trip for many assets is illustrated below.

In fact, the price level of the S&P 500 (US Large Company Stocks above) was 4766 on 1/1/2022 and 4770 on 1/1/2024, about as flat as you will get. Essentially all the return over that period came from dividends.

The Siren Song of Short-Term Rates

We entered 2023 with 1-year treasury rates and CD rates approaching 5%, and a few months in we surpassed 5%. With a tough 2022 and slow start to 2023, the siren song of a safe 5% return became too hard for some investors to ignore. It was a great move for investors shorter-term money that was otherwise still making nearly nothing in some large bank savings accounts, however, some investors also gave into the temptation selling stocks that were longer-term in nature and moving that money for the certain 5% return.

After experiencing such a rough 2022, this sense of certainty felt good to many investors at the time. However, 2023 ended up being just another example of many for why deviating from a long-term plan in the name of short-term comfort is usually never the right decision. As you saw earlier, major stock categories went on to return 3-to-5 times the return of short-term treasuries. Had an investor sold global stocks after the losses in 2022 and put that money into short-term treasuries, they would have experienced a cumulative loss of -14.2%. As mutual fund manager Rob Arnott likes to say “In investing, what is comfortable is rarely profitable”.

Election Season – Politics & Portfolios Don’t Mix

In my experience, one of the most persistent myths I see among investors is the belief that elections significantly influence broad market trends. Despite endless historical data showing otherwise, this misconception never goes away.

This hard held belief is understandable though. It is very easy to make a narrative for why market trends would be driven by elections…and the media loves that because they know their audience wants to hear it. Even better, when these narratives fail to materialize, it is just as easy to create a new narrative explaining away the old narrative. This cycle of narrative creation and revision is unfortunately endless, and an easy narrative can be tailored to anyone’s political beliefs.

While political events like elections can create short-term market volatility as investors react to uncertainties and policy expectations, the path of world economies and larger global trends are much more powerful than the current sitting presidents and politicians.

History shows time and time again that regardless of political persuasion, there is no reason to make short-sighted moves around election periods, as shown below.

Most often there are much bigger underlying economic situations unfolding during election years rather than the election themselves driving returns. Consider 2020 (Covid), 2008 (the global financial crisis) and 2000 (start of the dot-com bubble).

Two more recent historical examples of the folly of making politically motivated investment decisions comes from the Presidency of Barack Obama (A Democrat) and Donald Trump (A Republican). During the elections of both, supporters of the opposing party were certain that they would lead us to catastrophic market outcomes. Republicans argued that it was Obama’s tax policies that would ruin the market and Democrats argued that Trump’s trade policies would tank the market. It turns out that they were the 3rd and 4th best presidential terms for the stock market respectively. Markets returned 13.8% per year over Obama’s 8-year tenure and 13.7% per year under Trump’s 4-year tenure. They were only topped by Calvin Coolidge at 26.1% per year during the roaring 20s and Bill Clinton at 15.2% per year7.

History has shown that markets have thrived under various political landscapes. While it is important to stay informed about political events and their potential impacts, making politically motivated investment decisions is rarely in an investor’s best interest. It is important to discern between short-term political and media narratives and the much more powerful underlying currents that truly drive the markets.

The Way Forward

Dramatic ups and downs of the markets, as we have seen over the last 2 years, are just as unpredictable as they are certain. This is why the importance of a diversified portfolio cannot be overstated, but equally important is the fortitude to stay committed through the whole journey.

While we cannot eliminate risk, we can help manage it. On the path to meeting your long-term objectives your portfolios are designed to navigate the inevitable recessions and bear markets, but they cannot avoid them. We continue to be encouraged by this higher interest rate environment and the investment opportunities it has provided for our active managers.

As always, we are here to serve you. Don’t hesitate to reach out should you have any questions or concerns.

Paul R. Ried, MBA, CFP® | Timothy R. Kimmel, CFP® |

|

|

Prepared By:

Adam Jordan, CIMA®, AAMS®, IACCP®

Director of Investments/ CCO

Registered Principal*

1 – S&P 500 index 2 – Russell 2000 index 3 – MSCI All Country World Index ex US 4 – MSCI All Country World Index

5 – Bloomberg Aggregate Bond TR Index 6 – Bloomberg Short Treasury TR index

7 – Returns based off of Presidential inauguration dates https://www.kiplinger.com/investing/602714/best-and-worst-presidents-according-to-the-stock-market

Opinions expressed are not intended as investment advice or to predict future performance. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. All economic and performance information is historical and not indicative of future results. No investment strategy can ensure profits or protect against loss. The return and principal value of bonds fluctuate with changes in market conditions. If bonds are not held to maturity, they may be worth more or less than their original value. Investors cannot invest directly in indexes. Past performance does not guarantee future results.