February 2026 Market Commentary

February 4, 2026

It has been a while since our last formal market commentary. Not because there has been a shortage of headlines—if anything, it has been quite the opposite. Sometimes, when markets are flooded with narratives and opinions, the most valuable perspective comes from stepping back and remembering that not every development requires a response.

The challenge for investors is that the moments when action feels most urgent are often the moments when patience is most valuable. Much of modern investing is built around the illusion that more information always leads to better outcomes. History suggests that investors are rarely hurt by missing a headline, but are often hurt by acting on the wrong one.

Preparation & Patience Pay

In hindsight, the market reaction early last year to tariff announcements followed a familiar pattern and underscores the importance of preparation and patience. The experience was oddly similar to the COVID related sell-off in 2020. While the magnitude of the declines differed, the pattern itself was unmistakable.

In both cases, the market peaked on February 19th and fell sharply in under two months. In 2020, the S&P 500 declined 34% over 33 days, while last year it fell 19% over 48 days. Despite the uncertainty, markets recovered far more quickly than most expected. In both episodes, the S&P 500 had fully recovered its losses by the summer and went on to finish the year with strong double-digit gains, ending 2020 up 18.4% and last year up 17.9%.

What is most instructive about these episodes is not the speed or severity of the declines, or even how quickly markets began to look past them. It is that the bulk of the recovery occurred while uncertainty remained elevated and the underlying concerns were still far from resolved. Capturing those returns required resisting reactionary responses at precisely the moment they felt most justified.

Patience should not be confused with complacency. Being patient and staying disciplined does not mean ignoring developments or pretending that policy shifts, trade dynamics, or geopolitical changes don’t matter. It means recognizing that their economic and investment implications tend to unfold over years, not days.

Investing with this perspective shifts the focus away from short-term reactions and toward preparation. Successful investing is not about reacting to the last headline or wagering on the next one, but about building portfolios designed to navigate change as it plays out over full market cycles.

When Returns & Emotions Run High

We have now experienced three years of strong stock market returns. After several years of gains, it is not unusual for investor emotions to diverge into two camps. For some, higher prices– accompanied with higher valuations and economic indicators that begin losing momentum–can make investors uncomfortable and head for the sidelines, disengaging from their plan. For others, the price gains from the previous years can trigger the opposite reaction…a feeling of having missed out and a temptation to become more aggressive in an effort to catch up.

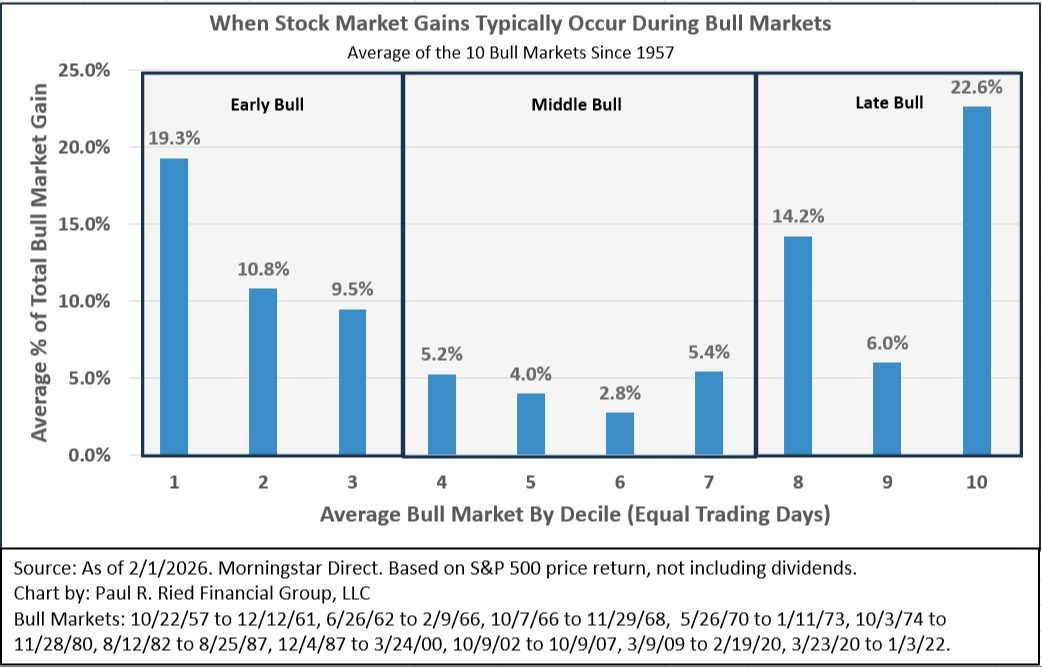

The irony of bull markets is that the moments when investors feel the most uncomfortable or emotionally charged are often the times that matter most for capturing returns. History shows, as you can see in the chart below, these emotionally charged periods at both the beginning and the end of bull markets are often when a disproportionate share of returns are generated, even though they rarely feel like comfortable times to be invested.

As shown, more than 20% of the total gains generated during the average bull market occur in the final 10% of its trading days. Similarly, nearly 20% of gains occur during the first 10% of days in a bull market, often before confidence has returned. Taken together, roughly 42% of all gains from the average bull market take place at the very beginning and very end of the cycle.

The reality is that we never know how close we are to the end of a bull market, or whether a new bull market has even begun, until well after the fact. Investors who step aside late in a bull market risk missing the final phase of returns, and those who exit during a downturn often struggle to re-enter early enough to participate in the next recovery. In practice, this means that investors that try to time the market must be right twice, knowing when to get out and when to get back in, an outcome that history suggests is far more difficult than it sounds.

While extreme market movements often trigger emotional responses, volatility can also serve a constructive purpose. Within a disciplined framework of a well-diversified portfolio, rebalancing provides a systematic way to manage risk and take advantage of opportunities by trimming areas of strength and reallocating to areas that continue to offer value. We believe the key is designing portfolios to weather the ups and downs of full market cycles, rather than trying to time them.

The Midterm Anomaly

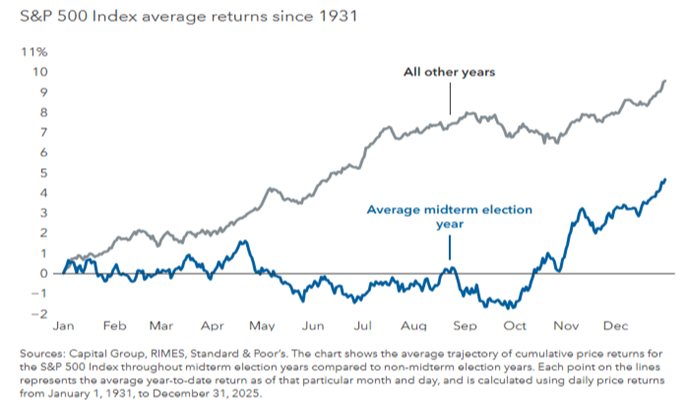

Historically speaking, on average, midterm election years tend to be the worst years for the stock market with an average price return of 4.7% vs 9.6% for all other years. Even Presidential Election years are quite a bit higher at 8.1%1.

Now granted, some of this is just statistical noise, with many factors affecting returns that are completely unrelated to the well documented Presidential Election Cycle Theory.

However, as you can see below, the general path of midterm election years is quite distinct from other years. On average the markets are negative heading into October and about flat heading into November.

Interestingly, the markets don't seem to care what the outcome is, it just cares that there was an outcome and the election is out of the way. The relief rally is quite pronounced. In fact, the S&P 500 has been positive in the 12 months following the midterms during every one of the 20 midterm elections since the Second World War, with an average price return over 14%1.

While the sluggish midterm stock market is definitely a pattern, it is far from a certainty. Averages have a way of hiding outliers and while the average price return was 4.7% during midterm election years…the range was as high as +45% in 1954 and as low as -30% in 1974.

Patience Is Not Complacency

This distinction—between patience and complacency—becomes especially important when considering today’s headlines. The economic environment we face today is in fact unique, although that is usually always the case in one way or another. However, we are experiencing genuinely significant geopolitical and trade shifts. After a year of escalating U.S. tariffs and threats, America’s longstanding allies and trade partners have begun striking deals among themselves to reduce reliance on the United States.

From the EU, Japan, Canada and the UK, they are all actively diversifying trade ties and, in some cases, even reducing dollar exposure in the global markets. The EU recently finalized a landmark free trade agreement with India that had been stalled for almost two decades, as well as expanded trade agreements with South American countries. Canada and the UK have also recently deepened trade ties with China.

These developments matter because they represent a structural shift. Companies and governments worldwide are actively reworking supply chains and reorganizing production…. Changes that will not be resolved in a quarter or two, but will unfold over years.

This is where the distinction between patience and complacency is key. Complacency is the easy route. Complacency is ignoring change because responding thoughtfully requires effort. Patience, on the other hand, is active. It requires ongoing assessment, discipline, and adjustment when necessary, without reacting impulsively.

Patience in investing does not mean standing still. It means responding to change on the appropriate time horizon. It reflects a commitment to maintaining investment exposure through periods of uncertainty while managing risk thoughtfully.

At the portfolio level, this means maintaining diversification across asset classes, regions, and investment styles, while rebalancing as conditions evolve to take advantage of relative value. Beneath the surface of the portfolios, our underlying managers are continuously evaluating opportunities, assessing valuations, comparing domestic and international markets, and adjusting exposures as fundamentals change. This all happens incrementally and deliberately, not in response to any single headline.

Keeping Your Plan the Priority

As we look ahead, we know the markets will continue to deliver the usual mix of noise, narratives, and unexpected headlines. Keeping your plan the priority means staying disciplined even when emotions run high…. recognizing that some of the most meaningful periods for long-term returns occur exactly when confidence feels lowest.

Above all, keeping your plan the priority means remaining committed to your long-term goals and the plan that was put in place to reach them. Thank you for your continued trust. As always, we are here to answer any questions you have as they arise.

Prepared By:

Adam Jordan, CIMA®, AAMS®, IACCP®

Director of Investments/ CCO

Opinions expressed are not intended as investment advice or to predict future performance. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. All economic and performance information is historical and not indicative of future results. No investment strategy can ensure profits or protect against loss. Diversification does not assure a profit or protect against loss in declining markets, it is a method to help manage risk. Past performance does not guarantee future results. Investors cannot invest directly in indexes Opinions about political, economic and market trends are based on current views and are subject to change without notice. References to specific indexes, sectors or asset classes are for informational purposes only and do not represent recommendations to buy or sell any security.

www.capitalgroup.com/pcs/insights/articles/midterm-elections-markets-5-charts-2026.html

1 – Ycharts, Carson Investment Research 1/23/2025 & 11/7/2023